Credit: Your Financial Foundation

Credit: Your Financial Foundation

Credit is your financial foundation. It plays a vital role in personal finance, impacting everything from lender approvals, interest rates, and even employment opportunities. Having a good understanding of credit and how it all works can help you make informed financial decisions. One of the most critical aspects of credit is a 3 digit number that represents your creditworthiness, commonly referred to as your Credit Score. Let's dive deep into what credit is, the credit score ranges and what they mean, who reports your scores, and examine the factors that affect your score.

What is Credit?

At the very core, credit is an agreement where a lender provides money or resources to a borrower with the expectation of repaying it back, typically with added interest. Common examples of these transactions are credit cards, loans, mortgages, etc. When you borrow money from a lender and pay it back accordingly, you create a Credit History which is a record of how you've handled debt. This helps lenders decide whether or not to work with you.

Your Credit Score

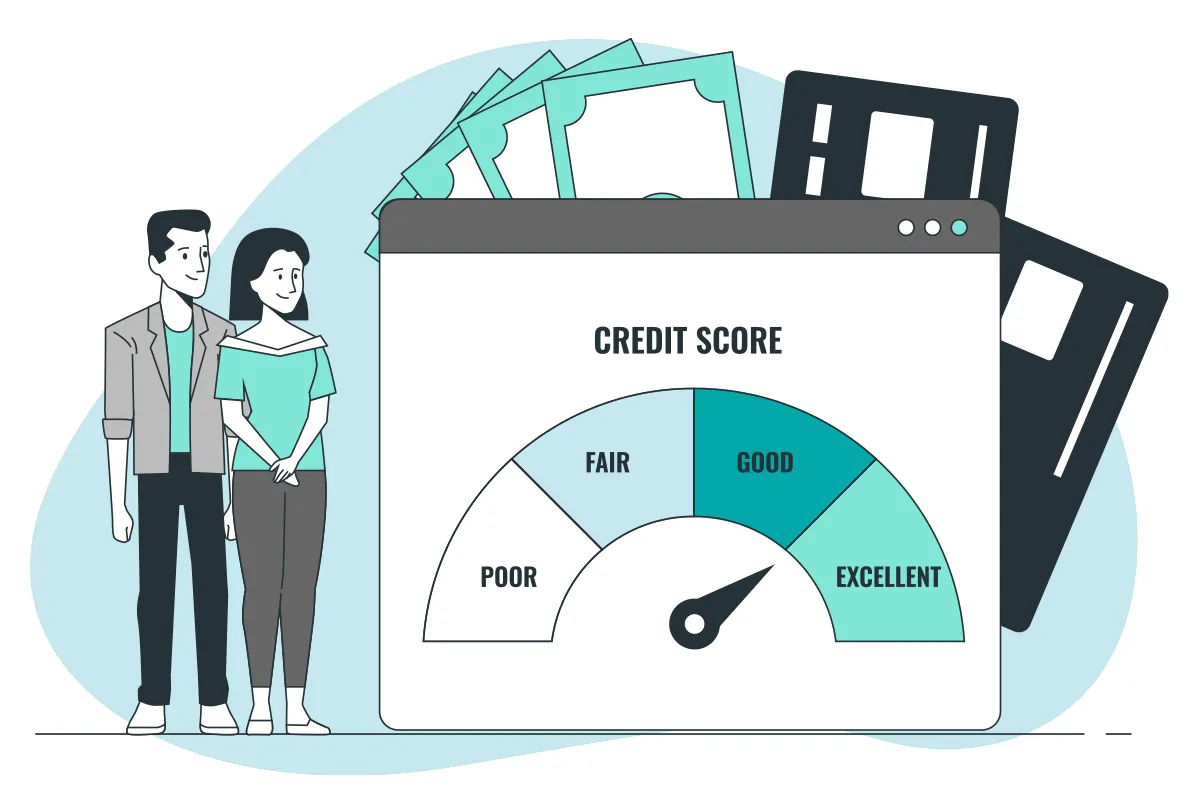

A credit score is a numerical representation of your creditworthiness. This score typically ranges from 300 to 850. Lenders use this score to assess how likely you are to repay borrowed money on an agreed time period. The higher the score, the more trustworthy you appear to lenders, in which they may offer better terms and interest rates.

While there are several different credit scoring systems, the most commonly used are FICO Score and VantageScore. They both account for similar factors but the score they weight may vary.

What are the Credit Score Ranges?

Credit scores typically fall into five categories, each representing a different level of creditworthiness. Let's take a look below:

300 to 579: Poor Credit - A score in this range suggests a history of financial mismanagement such as missed payments, defaulting on loans, or high credit card utilization. Borrowers with poor credit usually face difficulties of getting approved from lenders and may only qualify for loans with very high interest rates.

580 to 669: Fair Credit - In this range, your credit is still considered subprime. Lenders may view you as a risk but still may qualify you. However, you'll most likely still pay higher interest rates.

670 to 739: Good Credit - This range is generally seen as responsible financial management. People with good credit can qualify for most lender products with reasonable rates.

740 to 799: Very Good Credit - With this range, you are seen as a low-risk borrower among lenders. You can expect to receive favorable interest rates and terms.

800 to 850: Exceptional Credit - This is the highest range that shows lenders you have excellent credit management. Borrowers here often receive the best possible rates and terms.

What Affects Your Credit Score?

There are 5 key factors that influence your score, and each are weighed differently. Understanding these factors can help you maintain or improve your score. Let's review them below:

Payment History (35%) - Your payment history is the most significant factor affecting your score. Lenders want to see that you are responsible and pay your debts on time. Late or missed payments can damage your score while a history of on-time payments can boost it.

Amounts Owed (30%) - Also known as credit utilization. This refers to the amount of credit you are using compared to the total amount available to you. A high credit utilization tells lenders that you are overspending and at a higher risk of defaulting, while a low credit utilization shows that you are able to manage your finances. A utilization below 30% is generally recommended for maintaining a good score.

Credit Age (15%) - The length of time you've been using credit also plays a role in your score. Longer credit history provides more information about your financial behavior and is generally better for your score. Lenders look at the age of your oldest and newest accounts including the average age of all your accounts.

Credit Mix (10%) - Having a variety of credit products such as credit cards, loans, and retail accounts can positively affect your score. It shows lenders that you can handle different types of credit responsibly.

New Credit (10%) - Opening new accounts in a short period of time can hurt your score. Each time you apply for credit, it results in an "inquiry". Inquiries are broken down into soft inquiries or hard inquiries. Soft inquiries typically don't affect your score while hard inquiries are the ones that can lower your score. Regardless of which, lenders take into account these inquiries to evaluate risk.

How to Maintain or Improve Your Score?

There are a few tips that you can use to maintain or even improve your score. Although some may seem obvious, there additional methods to keep in mind that will help you overall.

Pay Bills on Time: While this is the most obvious, this can sometimes be missed. Your payment history has the biggest impact on your score. Always aim to pay at least the minimum amount due on time.

Keep Utilization Low: Using less than 30% of your available credit is a good method of managing your score. If possible pay off your balances in full each month.

Don't Close Old Accounts: Even if you don't use an old credit card, keeping it open can help the length of your credit history. This is something that can easily be overlooked.

Limit Credit Applications: Only apply for credit when you need it to avoid hard inquiries. In this day and age, lenders may offer soft inquiry products that may not affect your score. However, avoiding opening new credit accounts when not needed can help you better manage your finances.

Monitor Your Credit Report: Checking your credit report regularly helps give you a clear picture on your overall history. These reports may also have errors or suspicious activity in which you are able to dispute any inaccuracies.

Who Reports Your Credit History?

In the U.S., there are 3 major credit bureaus that play a critical role in the credit reporting system. These bureaus are Equifax, Experian, and TransUnion. These agencies are responsible for collecting, maintaining, and distributing credit information on millions of people. When you apply for a credit card, loan, or even a job, lenders and other organizations usually rely on reports from this bureaus to analyze your creditworthiness.

At this point you might be wondering why there are 3 bureaus. Let's review below:

Lender Preferences: Different lenders and financial institutions report to one or more of the bureaus based on their preference or even partnerships. Some may report to all three while some may only report to one or two.

Regional Differences: Some credit bureaus may have stronger relationships with certain lenders in specific regions or industries.

Competition: The three credit bureaus operate independently of each other and are separate companies, which leads to competition. This competition brings innovation in the services they offer such as credit monitoring, fraud protection, and educational tools.

Your Financial Foundation

Understanding how credit works and what factors affect your credit score is crucial for financial success. By managing credit responsibly, you can build and maintain a strong credit score. Moving up the ranks of the system and obtaining the highest credit score you can possibly have will open doors to better financial opportunities and higher limits with favorable terms and rates.

With this knowledge, you're better equipped to navigate the world of credit and make decisions that benefit your overall financial health.

Ready to see what funding opportunities your credit can get you? Let's chat.